Today’s Sponsor

By the time a small-cap stock is making headlines, the early opportunity is already gone. The real setups develop quietly — in the companies building the infrastructure and technology behind the trend, before the crowd arrives. That's exactly where we're looking right now.

We've identified five under-the-radar profiles showing early signals — shifting volume, momentum, and positioning — that historically appear before broader attention moves in. Our latest free report breaks down how we spot these setups and names the five companies currently on our watchlist.

Get the Free Watchlist ReportWe encourage readers to perform their own research and due diligence on any information we provide. By clicking the link above, you will automatically be subscribed to the Krypton Street Newsletter. To view our privacy policy, visit lifewatermedia.com/privacy-policy.

Record IPO meets a risk-on tape. Washington keeps playing with supply chains. Cybercrime goes corporate. Midwest storms remind you why insurers trade like macros.

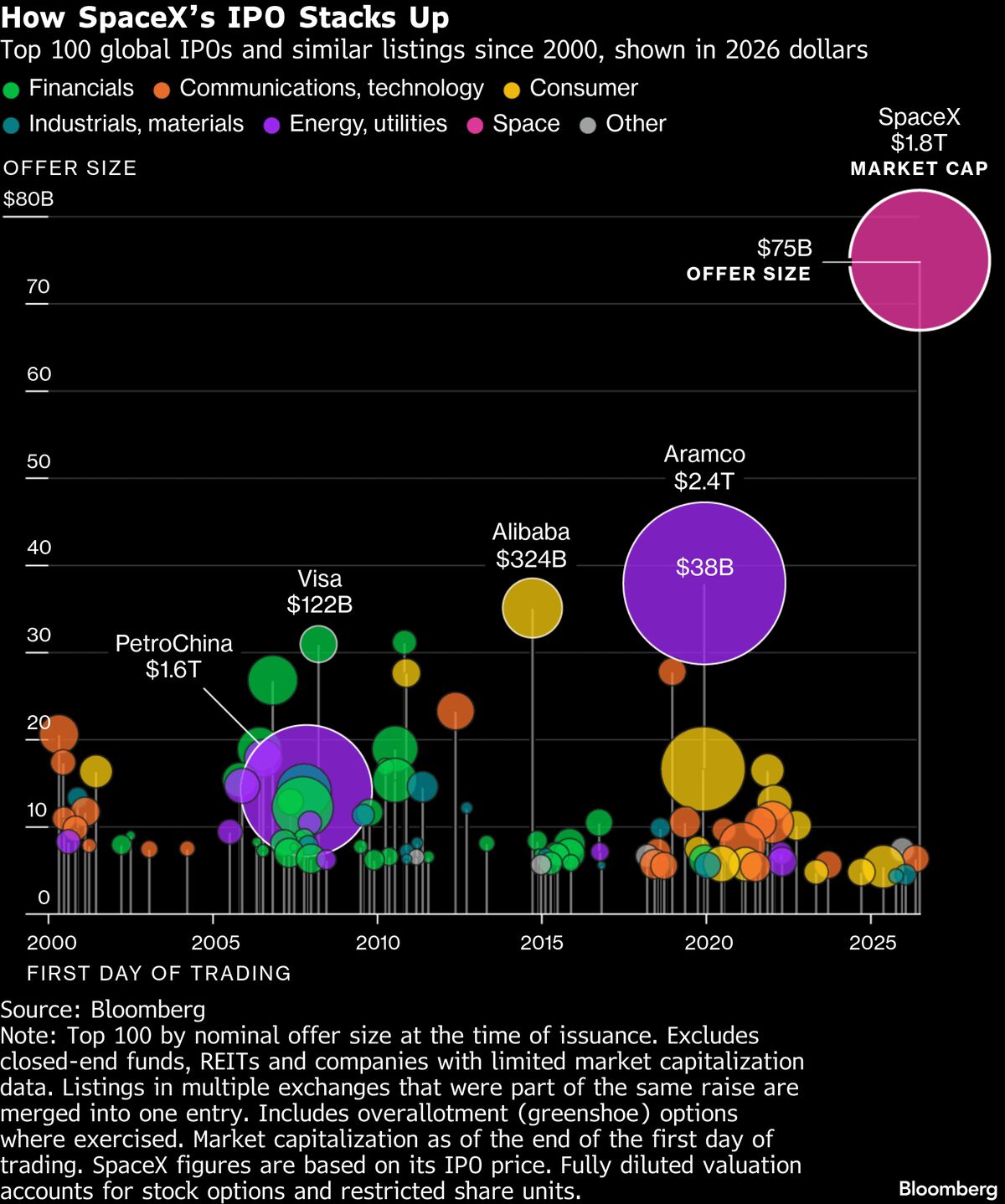

Image via Bloomberg

SpaceX Prints a $75B IPO. Now It Has To Trade.

SpaceX just pulled off a $75 billion IPO — the biggest on record — and instantly graduated from "private mythology" to "public P&L." The easy part was getting the paper sold. The hard part starts at the open: real liquidity, real price discovery, and a market that will punish any mismatch between story and numbers.

The tape will treat this like a referendum on the whole "future tech" complex: launch cadence, Starlink economics, defense revenue durability, and capex discipline. If it holds the bid, it resets risk appetite for everything adjacent — aerospace, satcom, defense tech, and the late-stage venture names lining up behind it. If it wobbles, it’s not just SpaceX that gets repriced; it’s the multiple the market is willing to pay for long-duration narratives.

📈 Fred's Take: This is a liquidity event disguised as a tech event. If SpaceX opens strong and stays strong, it loosens financial conditions at the margin: expect beta to catch a bid and the IPO window to crack open wider. If it trades like a busted unicorn, you’ll see the hangover hit momentum, small caps, and the next wave of "AI + hardware" capital raises.

Image via ZeroHedge

Futures Up on Iran Peace Chatter. Oil Down. Risk On — With One Giant Asterisk.

Index futures are higher and global markets are leaning risk-on as fresh Iran peace hopes make the rounds. Crude is sliding, which is doing what it always does: easing headline inflation pressure and giving equities permission to breathe. When oil backs off, the market immediately starts daydreaming about friendlier CPI prints and a less-hawkish rates path.

But today’s tape is also going to be captive to SpaceX price action. A record IPO debut on a "peace + lower oil" morning is rocket fuel for animal spirits — until it isn’t. If the Iran headlines fade or oil snaps back, the risk bid can evaporate fast, especially with positioning already tilted toward "good news stays good."

📈 Fred's Take: Lower oil is the cleanest impulse for stocks and the ugliest impulse for energy. If crude keeps bleeding, watch breakevens fall and long duration catch a bid — that’s where the real upside torque sits. Don’t confuse a headline-driven oil dip with a structural peace dividend; this market has been rugged by Middle East “progress” a hundred times.

Google Sues an "Organized" China Cyber Ring. Markets Should Price This Like Ongoing Capex.

Google filed a lawsuit targeting what it calls a Chinese "organized cybercrime operation," warning that criminals increasingly use AI to scale attacks. Translation: the defense perimeter is now an arms race, and AI just made the attackers cheaper, faster, and more persistent. This isn’t a one-off legal story — it’s an operating reality for every enterprise with a balance sheet and a network.

For markets, the key is where the spend goes. Companies don’t debate cybersecurity budgets after a high-profile incident; they sign contracts. That funnels dollars to security vendors, identity platforms, cloud hardening, and managed services — while quietly raising the long-run cost base for everyone else. Lawsuits are theater; the real response is recurring opex.

📈 Fred's Take: AI doesn’t just boost productivity — it boosts crime ROI. That means cybersecurity stays a secular growth pocket even if the broader tech multiple compresses. If you’re hunting durable cash flows, look for security names with net retention and pricing power; the "we’ll cut spend" story dies the first time a CFO sees a breach invoice.

Image via National Review

Tariffs 2.0: The USMCA Isn’t a Bloc If Washington Treats It Like a Suggestion.

A National Review piece lays out the problem with Trump’s replacement tariffs: you can’t run North America as an integrated production zone while constantly yanking the policy wheel. USMCA only works when firms believe the rules won’t change mid-cycle. If commitments become optional, supply chains don’t "adjust" — they re-price risk and move investment elsewhere.

Markets care because tariffs aren’t just a trade policy; they’re a volatility policy. They hit margins through input costs, they distort capex plans, and they invite retaliation that shows up in earnings calls six months later. And they complicate the Fed’s job by injecting cost-push inflation into a system that wants disinflation.

📈 Fred's Take: Tariffs are a tax that shows up as higher prices, lower margins, or both — pick your poison. The winners are the politically protected domestic producers; the losers are manufacturers with cross-border parts lists and retailers with thin gross margins. If this rhetoric turns into implemented policy, expect inflation hedges (gold, energy) to stay bid and expect multinationals to guide more conservatively.

Image via AP

Tornado Damage in IL/IN: The Quiet Macro Trade Is Insurance, Not Weather.

Officials are searching tornado-damaged areas after strong storms hit Illinois and Indiana, with reports of significant damage across multiple communities. Beyond the human cost, the market read-through is straightforward: more severe weather events mean more claims, more reinsurance stress, and more pressure on premiums.

When catastrophe frequency rises, insurers don’t absorb it out of kindness — they reprice. That feeds into housing affordability, commercial real estate operating costs, municipal budgets, and ultimately consumer inflation baskets via higher services costs. Weather is increasingly a macro variable because it changes the cost of doing business.

📈 Fred's Take: The immediate trade isn’t "sell everything" — it’s watch the insurance complex and any regionally concentrated exposures. Higher premiums are sticky and they behave like a slow-motion rate hike on households and small businesses. If storms keep stacking, reinsurance pricing will do what it always does: jump, then stay elevated longer than people expect.

📎 AP

That’s the tape: SpaceX sets the tone, oil sets the inflation mood, and policy sets the risk premium. Trade what’s in front of you, not what you wish Washington meant. — Fred Frost, Morning Bullets

— Fred Frost