Today’s Sponsor

Markets are shifting — and most investors are missing it. The free Market Shift Report + Real-Time Watchlist breaks down exactly what's moving right now: policy impacts on economic trends, the return of supply-chain concerns, and what mixed consumer signals mean for the next quarter.

This complimentary report is only available for a limited time while these patterns are still developing. Don't get caught flat-footed — access it now before it's gone.

Get the Free Market Shift ReportWe encourage readers to perform their own research and due diligence on any information provided. By clicking the link above, you will automatically be subscribed to the Market Crux Newsletter. Privacy Policy

Credit gates are going up, GLP-1s go mainstream, Graham faces runoff math, bitcoin puke trades spill into equities, and Europe’s fighter jet program fractures — all with real portfolio consequences.

Image via TheStreet

Private Credit Discovers the “T+Never” Feature

Blackstone and Cliffwater are capping withdrawals as credit markets get jumpy, and the timing tells you everything. Private credit sold itself as bond-like income with equity-like returns and cash-like access. That last part was always marketing.

When redemptions accelerate, these vehicles don’t “find liquidity” — they ration it. That’s not a scandal, it’s the product design. But it becomes a problem when investors treated it like a savings account and advisors sold it like one.

The real issue isn’t this week’s gates. It’s the next quarter’s mark-downs. Private credit pricing is slow, negotiated, and model-driven; public markets reprice in minutes. That gap is where the pain hides until it doesn’t.

📈 Fred's Take: If withdrawals are being capped, your risk isn’t just illiquidity — it’s stale valuations about to catch up. This is a quiet tightening of financial conditions: less cash coming out means less cash going into everything else. Own liquid credit over “promise-you-can-get-out” credit until spreads settle and marks are believable again.

Image via ZeroHedge

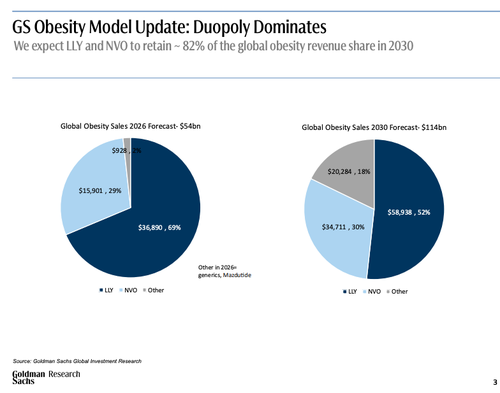

Goldman Sees $114B Obesity Drug Market: That’s a Supply Chain Trade, Not Just Pharma

Goldman lifted its obesity drug market forecast to $114B by 2030 as oral GLP-1s move toward mass-market distribution. Translation: this category is shifting from boutique injectables to something that looks like daily chronic therapy at scale.

That changes who wins. It’s no longer only about headline trial results — it’s about manufacturing capacity, pill-formulation execution, payer coverage, and adherence. The margin stack migrates from “breakthrough drug scarcity” toward “industrialized volume.”

Second-order effects matter more than the press release. If oral GLP-1s broaden access, you get sustained pressure on parts of food, alcohol, and certain medtech utilization patterns — but it won’t be linear, and the market will overtrade the narrative both ways.

📈 Fred's Take: The easy trade was owning the incumbents. The next trade is owning the picks-and-shovels: CDMOs, packaging, and the distribution/benefit-management plumbing that can handle scale. Also: don’t short every consumer brand on a headline — wait for payer coverage data and refill behavior; adherence will decide the true TAM.

Image via Washington Examiner

Graham Runoff Risk: Markets Don’t Care—Until Committee Math Does

A bloc of undecided voters could push Sen. Lindsey Graham into his first-ever runoff in South Carolina’s GOP primary. That’s less about ideology and more about fatigue: long-tenured incumbents are now forced to campaign like challengers.

On the tape, a runoff itself is noise. The signal is what it says about party cohesion heading into the mid-cycle calendar and how much political oxygen gets pulled away from policy. When incumbents have to fight at home, legislative bandwidth shrinks.

For investors, the practical channel is committee seniority and influence. Graham has had a seat at big national-security and spending conversations for years. If his position gets politically constrained, expect more headline volatility and less predictability around defense and appropriations timing.

📈 Fred's Take: This isn’t a “sell stocks” event. It’s a reminder that Washington’s base politics are getting more transactional, which usually means messier budgeting and more stopgap funding. Price a slightly higher probability of continuing resolutions and procurement delays — bad for small defense suppliers, tolerable for the primes.

Bitcoin Gets Hit, Traders Rotate the Damage into Stocks—And Someone’s Buying the Dip Hard

Bitcoin’s latest brutal sell-off didn’t scare traders out of the ecosystem — it pushed them into it. Volumes spiked in bitcoin-linked equities and derivatives as the crowd re-expressed the same view through different tickers: miners, proxy tech names, and levered products.

That’s classic risk transfer. When spot gets ugly, people either hedge with liquid listed names or take convex shots where market makers can warehouse flow. It also means “crypto contagion” will show up in equity factor land: momentum, high beta, and anything with a retail-heavy options complex.

One notable feature: alongside the panic, there was a big bullish bet. That’s not heroism — it’s positioning. These drawdowns are where long-dated call buyers show up because implied volatility stays elevated even after the initial flush.

📈 Fred's Take: Watch the miners and the proxy basket as your real-time stress gauge — they’ll lead spot both down and up. If you’re long, define your risk: this tape will keep punishing leverage and rewarding patience. If you’re looking to add, scale in on volatility compression, not on the first red candle that feels “cheap.”

📎 CNBC

Image via Bloomberg

Europe’s Fighter Jet Program Splinters: Defense Budgets Up, Execution Risk Up More

Germany is looking for new partners to salvage Europe’s next-gen fighter effort, potentially moving forward with Spain and Sweden without France. That’s a big tell: the politics of industrial policy are colliding with the urgency of rearmament.

Defense spending can be bullish, but program structure matters. When the consortium fractures, you get duplicated R&D, procurement delays, and contract uncertainty — all while cost inflation and supply-chain constraints stay sticky. The market loves the headline “more defense,” then wakes up to “more cost overruns.”

If Berlin reconfigures partners, expect a reshuffling of workshare: avionics, engines, composites, and systems integration. That creates winners and losers across European primes and a second tier of suppliers that are far more sensitive to schedule slips.

📈 Fred's Take: This is bullish for near-term orders in existing platforms and munitions, bearish for long-duration “big new jet” timelines. Execution risk is the hidden tax on European defense trades — you want cash-flow visibility, not PowerPoint air superiority. Favor firms tied to current production lines and sustainment over moonshot development programs.

That’s the board. Liquidity is the only thing that never lies — in credit, in crypto, and in politics.

— Fred Frost