Today’s Sponsor

Oil markets are shifting as Venezuela's disruption removes critical barrels while spare capacity shrinks. Supply pressure is building before headlines catch up — and smart traders are positioning now.

Our exclusive briefing reveals three energy stocks emerging from this supply shock, plus the key signals to monitor as this setup evolves. This is about preparation, not prediction.

Get the Free Oil Trading ReportBy following the links above, you're opting in to receive valuable updates from Wealthiest Investor News plus 2 bonus subscriptions. Your privacy is important to us. You can unsubscribe anytime. See our privacy policy for details.

Five tells before the bell: luxury is discounting, energy risk is repricing, NATO is fraying, cars are unaffordable, and DOJ is turning into a trade.

Image via Bloomberg

De Beers Blinks: Diamond Price Cuts Signal the Cartel Is Losing Control

De Beers just dropped some of its deepest official price cuts in years. Translation: the “sightholder” club is shrinking, inventories are heavy, and the gap between De Beers’ list prices and real-world clearing prices finally became impossible to defend.

This isn’t only about cyclical demand. Lab-grown keeps stealing the mid-market, China’s luxury appetite is still uneven, and higher-for-longer rates have crushed discretionary financing. When the dominant price-setter starts chasing the market down, the illusion of scarcity is over.

Watch the knock-on: Botswana/Namibia fiscal math gets tighter, luxury supply chains get uglier, and any company with exposure to natural stones faces margin compression until inventories clear.

📈 Fred's Take: This is a classic “price discovery event” in a controlled market. If you own luxury equities, stop pretending diamonds are an inflation hedge—this is deflation hitting the vanity complex. The trade is simple: treat natural diamonds like any other over-inventoried consumer good when real rates stay high.

Trump Lands in Turkey With NATO Under Stress: Markets Hear “Less U.S. Patience”

Trump arrived in Turkey with NATO strained by Russian attacks and a louder U.S. message: allies need to carry more weight. CNBC notes he’s been venting about NATO members not helping clear the Strait of Hormuz during the U.S. campaign against Iran—exactly the kind of grievance that hardens into policy.

The market angle isn’t the photo ops. It’s the probability distribution on security guarantees, burden-sharing, and whether U.S. support gets conditioned on spending and operational commitments. That shifts defense procurement, energy-route risk premiums, and the euro area’s fiscal posture.

If Europe has to rearm faster while also funding energy security, you’re looking at more issuance, stickier inflation in pockets, and higher term premium—especially if Washington turns transactional instead of automatic.

📈 Fred's Take: Geopolitics is becoming a line item again, not a headline. Defense contractors stay bid, but the bigger move is rates: higher European issuance and wider risk premiums feed directly into global duration. If you’re long long-dated bonds like it’s 2019, you’re on the wrong side of this regime.

📎 CNBC

Image via Fox Business

$770 a Month: The Car Payment Just Told You the Consumer Is Cornered

Average new car payments hit a record $770 per month, with auto loan debt up to $1.685 trillion—now larger than student loan balances. That’s not “strong demand.” That’s the price level colliding with the monthly budget.

This matters because autos sit at the intersection of manufacturing, credit, and consumer psychology. When payments are the pain point, buyers stretch terms, roll negative equity, and default rates creep. That’s how you get slower unit volumes, higher incentive spend, and a worsening loss curve for lenders.

Keep an eye on used-car prices and delinquency data. If used values soften while loan balances stay elevated, lenders tighten, approvals drop, and the whole chain goes risk-off fast.

📈 Fred's Take: The auto market is a credit story wearing a consumer costume. Automakers can manage production, but they can’t print affordability—banks decide that, and they’re tightening when losses rise. Expect pressure on subprime lenders and a widening gap between premium brands and everyone else.

Image via The Hill

1,200 DOJ Alums vs. Todd Blanche: The Confirmation Fight Becomes a Rule-of-Law Risk Premium

More than 1,200 former Justice Department employees urged senators to reject Todd Blanche’s attorney general nomination, arguing he’s unfit for the role. Big institutional pushback like this signals the confirmation won’t be clean, quick, or quiet.

Markets don’t trade “ethics.” They trade predictability. A DOJ seen as politicized—fairly or not—raises the volatility of enforcement: antitrust timelines, crypto cases, bank investigations, and corporate settlement calculus. That uncertainty becomes a tax on multiples, especially for companies living under regulatory microscopes.

The second-order effect is Washington bandwidth. The more oxygen this fight consumes, the less capacity there is for clean fiscal/immigration/energy policy—meaning more policy drift and more market whipsaw off headlines.

📈 Fred's Take: This is risk premium, not theater. If DOJ becomes a partisan battleground, enforcement becomes less predictable and more headline-driven—bad for deal-making and anything reliant on regulatory clarity (crypto, big tech, large banks). Trade it as “higher vol, wider spreads,” not as a one-day political spat.

📎 The Hill

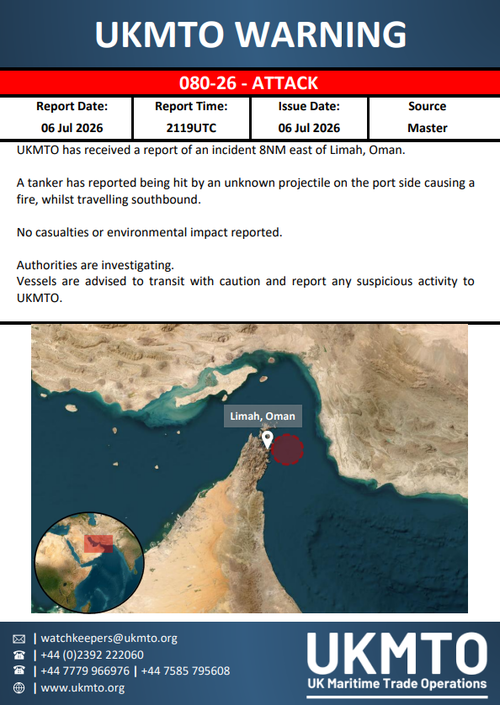

Image via ZeroHedge

Hormuz Just Lit Up: Iranian Strike on Qatari LNG Tanker Forces an Energy Reprice

A fully loaded Qatari LNG tanker was reportedly struck by a projectile near the Omani coast while exiting the Strait of Hormuz. That’s not a “shipping incident.” That’s a direct hit to the world’s most sensitive energy chokepoint.

The immediate market read is risk premium in crude and LNG, plus a jump in freight and insurance costs. The deeper read: Europe and Asia don’t have slack LNG logistics if Hormuz is contested—so the marginal molecule gets repriced, fast. Even if flows continue, the optionality value of supply security explodes.

Watch for knock-on effects in inflation prints, airline margins, and central bank tone. Energy shocks don’t need to last long to change rate expectations when the starting point is already tight financial conditions.

📈 Fred's Take: This is the kind of headline that moves from “geopolitical noise” to “macro input” in one trade. I’d expect energy and shipping to catch a bid, and I’d fade any rally in long-duration growth if oil rips—because the Fed doesn’t cut into an energy-driven inflation pulse. Gold and cash-like duration hedges make sense here; pretending this is contained is how portfolios get clipped.

That’s the tape: luxury is discounting, the consumer is financing, and Hormuz is rewriting the inflation math. Trade accordingly. — Fred Frost

— Fred Frost