Today’s Sponsor

Wall Street's been using ruthless, unemotional algorithms to run 80%+ of all stock trades — and that number keeps climbing. K.I.R.A. is the advanced AI engine built to level the playing field, giving everyday traders the same edge as the pros. It analyzes the market and hands you three distinct trade approaches — tailored to your risk tolerance — so you're never left guessing.

You don't have to take anyone's word for it. Fire up K.I.R.A. right now and see exactly what it surfaces for today's trades. The robots aren't waiting — and neither should you.

Access K.I.R.A. Now — See Today's TradesBy clicking the link above you agree to periodic updates from The TradingPub and its partners. Privacy Policy

Apple and Intel get a White House tailwind, Warsh rewires how markets read the Fed, and Israel/Iran theater keeps energy and defense bids alive even as crude fades this week.

Image via Fox Business

Apple + Intel, Made-in-America Chips: Trump Puts the Bid Under Onshoring

Trump says Apple will work with Intel on U.S. chip design and production. That’s not just an industrial-policy headline — it’s a supply-chain re-rate attempt. The White House is effectively telling the market: "We’re paying to de-risk China, and we want the capex here."

If Apple is serious about shifting more silicon work into the U.S. orbit, Intel gets what it’s been starved of for a decade: a marquee customer narrative that isn’t just foundry PowerPoints. But this will be slow, expensive, and full of execution landmines — yields, packaging capacity, tools, power, permitting, and the simple fact that leading-edge economics still love scale.

Watch the second-order winners: U.S. equipment, advanced packaging, specialty chemicals, grid/power buildout, and the states that can actually approve projects without a lawsuit. Also watch margins. Apple doesn’t like cost creep, and Intel doesn’t like being forced to hit timelines it can’t control.

📈 Fred's Take: This is bullish for the "U.S. semiconductor complex" trade and neutral-to-slightly bearish for near-term hardware margins. Apple can absorb higher unit costs better than most, but the Street will punish any gross-margin wobble. Intel finally gets a real shot at credibility — if they miss, the stock will wear it for years.

Image via MarketWatch

Fed-Watching in the Warsh Era: Less Fortune-Telling, More Measuring

MarketWatch is right: Kevin Warsh is making Wall Street do the heavy lifting. The old game was decoding dovish adjectives and guessing the next dot-plot drift. The new game is closer to: "Show me the data that forces the Fed’s hand."

Two practical benchmarks matter more now than the vibe: where real rates sit versus realized inflation, and whether financial conditions are easing or tightening without the Fed’s permission. In plain English: if risk assets rip and credit spreads compress, Warsh doesn’t have to cut to keep the expansion going — he can sit and let markets do the work.

This is a regime shift for positioning. Cuts aren’t a moral right. They’re a response function. And Warsh is signaling that the bar is higher: inflation persistence gets punished, and frothy conditions don’t get rescued.

📈 Fred's Take: Stop trading speeches and start trading constraints. In this era, equities can rally without cuts — but the upside gets capped if real yields stay elevated. For portfolios, that’s a tilt toward quality cash flows, shorter-duration growth, and staying humble on long-duration bets that need a Fed put to work.

Image via Fox News

Trump Toys With a Netanyahu Endorsement — Israel Politics, Meet Your Risk Premium

Trump is dangling an endorsement in front of Netanyahu ahead of a crucial Israeli election, praising him while warning he needs to be "more rational." That’s a political lever, not a compliment. Trump is signaling he wants influence over the next phase of Israel’s decision-making — security posture, Gaza endgame, and how hard Israel pushes Iran’s proxies.

Markets should read this as: U.S.-Israel alignment is conditional and transactional. When endorsements turn into bargaining chips, it increases uncertainty around coordination, timing, and red lines. And uncertainty in the Middle East doesn’t stay local — it shows up in energy vol, defense orders, and safe-haven flows.

If Israel’s political path looks unstable into the election window, expect more headline gaps in crude and more defensive positioning in global risk assets, especially during thin summer liquidity.

📈 Fred's Take: This is not about personalities — it’s about policy volatility. The endorsement tease raises the odds of abrupt messaging shifts, and markets hate that. Keep some exposure to hedges that actually work in geopolitical spikes: defense, gold, and optionality in energy.

📎 Fox News

Image via The Hill

Israel-Lebanon Strikes Stress-Test the U.S.-Iran Track — Talks Slip, Risk Rises

Renewed Israel strikes tied to Lebanon/Hezbollah are testing the preliminary U.S.-Iran framework meant to kick off nuclear talks and prevent a slide back toward open conflict. Peace talks are being postponed — which is diplomat-speak for "the timeline is breaking."

When negotiations slip, the market’s default assumption becomes escalation risk until proven otherwise. That doesn’t always mean higher spot oil immediately, but it does mean higher implied vol, more upside skew in crude options, and a steadier bid for defense and cybersecurity as governments and proxies posture.

The bigger macro angle: any geopolitical flare that threatens shipping lanes or energy infrastructure tightens global financial conditions at the margin. That’s exactly the kind of external shock that complicates Warsh’s higher-bar stance on cuts.

📈 Fred's Take: This is a volatility story before it’s an inflation story — but it can become both fast. If talks keep sliding, energy hedges get more expensive and the market quietly reprices tail risk. I’d rather pay for protection when WTI is soft than chase it after the first real supply scare.

📎 The Hill

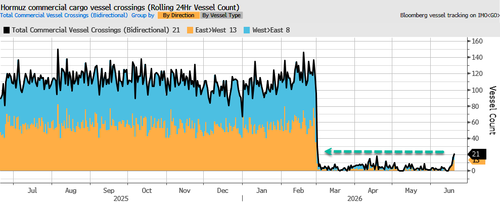

Image via ZeroHedge

Hormuz Traffic Pops, Iran Re-Tightens Rules — Don’t Confuse “Flows” With “Safety”

Ship traffic through the Strait of Hormuz rebounded to the highest level since the start of the war, even as Iran renews restrictions. That’s the push-pull: commerce wants to normalize, security reality keeps tightening. More boats in the lane doesn’t reduce risk — it concentrates it.

Oil is set to close lower this week with WTI down, but don’t let the weekly candle lull you. A busier Hormuz with fresh restrictions is how you get one incident turning into a pricing event: delays, insurance premiums, rerouting, and a sudden scramble for prompt barrels.

This is also why energy equities can diverge from crude. The sector trades the distribution of outcomes. When tail risk thickens, quality producers and midstream with resilient cash flows can catch a bid even if front-month futures drift.

📈 Fred's Take: Lower WTI with higher Hormuz friction is the market giving you a gift: cheaper hedges. The right move isn’t pounding crude spot — it’s owning asymmetry via options or selective energy names with real free cash flow. If an incident hits, you won’t have time to build protection at a fair price.

That’s the board. Trade the incentives, not the headlines. See you before the bell Monday.

— Fred Frost