Today’s Sponsor

Policy is already moving markets in 2026 — trade enforcement, regulatory shifts, and tax positioning are redirecting capital right now. Institutions reposition before the headlines catch up, and the window to act early is closing fast.

Our analysts identified 5 stocks showing real momentum tied directly to current administration policy themes — including the sectors benefiting most from domestic investment trends and regulatory tailwinds. Don't get left behind.

Get the Free Report Now(By following any of the links above, you're choosing to opt in to receive insightful updates from The Investment News Daily + 2 free bonus subscriptions! Your privacy is important to us. You can unsubscribe anytime. See our privacy policy for details.)

Politics is policy is price. Today’s tape: better growth than feared, louder populism on the ballot, fresh oil-supply fracture risk, and a summer melt-up riding good vibes and AI capex.

Image via Fox Business

GDP Prints 2.1%: The Economy Isn’t Rolling Over — It’s Re-Accelerating in AI Capex

Final Q1 GDP came in at 2.1%, ahead of the 1.6% consensus. The mix matters: equipment investment tied to AI and computing kept the capital-spending engine humming, and the consumer stayed in the fight.

This is the cleanest version of “productive inflation” you can get: businesses buying machines, chips, and software to squeeze more output per worker. It’s also the kind of growth print that keeps the Fed from cutting just because Wall Street wants it. If you were hoping for a rapid glide-path to easier financial conditions, this doesn’t help your case.

Markets will treat this as a Goldilocks datapoint until rates remind them who runs the room. Stronger real growth supports earnings, but it also props up the front end and keeps term premium sticky.

📈 Fred's Take: This is bullish for AI beneficiaries and broadly supportive for equities, but it’s bearish for “aggressive cuts” narratives. Expect rates to stay higher-for-longer than the cheerleaders want, which means the winners keep being cash-flowing growth and capex enablers — not long-duration junk. If you’re positioned for a quick dovish pivot, you’re leaning into the wind.

Image via National Review

NY Primaries Signal a Hard Left Turn — Markets Hear “More Spending, More Regulation”

National Review’s read on the New York primaries is blunt: the Democratic base is drifting from pragmatic coalition politics toward a more ideological, revolutionary wing. You don’t need to like the framing to understand the market implication: primaries drive personnel, personnel drive committees, and committees write the rules.

When the center of gravity shifts left, the platform shifts with it: more aggressive labor policy, higher corporate and capital taxes, louder antitrust posture, and a bigger appetite for fiscal programs. Even if none of it becomes law immediately, it changes the negotiating range — and that changes valuation multiples.

This is also a donor/reaction function. The further candidates run from the middle, the more business money flows to the other side or to “gridlock insurance.” Gridlock is often bullish; ideological momentum is volatility.

📈 Fred's Take: This is not about ideology. It’s about expected policy paths. If the party’s energy keeps moving left, you price a higher probability of tax/regulatory drag on mega-cap, healthcare, banks, energy, and private equity — and a higher probability of deficit-friendly spending that keeps real rates elevated. The trade isn’t panic; it’s selectivity and hedges: quality balance sheets, pricing power, and less Washington beta.

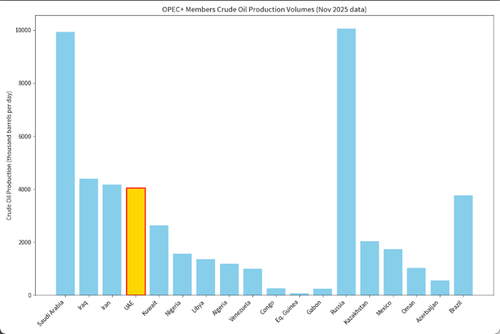

Image via ZeroHedge

Iraq Threatens to Walk from OPEC: That’s a Supply Shock Waiting to Happen

ZeroHedge flags Iraq firing a warning shot at OPEC: raise Baghdad’s production quota or risk Iraq abandoning the cartel. When a major producer starts talking exits, it’s not theater — it’s a signal that internal discipline is fraying.

OPEC works when members believe restraint pays. When budgets are stressed and politics are hot, cheating becomes rational. An Iraq exit (or even sustained quota defiance) is a two-way risk: it can flood the market near-term, but it can also trigger retaliation, fragmentation, and ultimately less coordinated supply management — which tends to increase volatility and fat-tail spikes.

Energy traders care less about the headlines and more about the reaction function: does Saudi enforce discipline, does OPEC+ absorb it, and how fast does non-OPEC supply respond. The range widens either way.

📈 Fred's Take: Oil volatility is back on the menu. Near-term, the market will lean “more barrels” and fade crude — until the geopolitics hits the bid and the curve re-prices risk premium. My playbook: don’t marry direction; own optionality. Energy equities with disciplined capital return beat hero futures calls when the cartel starts wobbling.

Summer Melt-Up: The Tape’s Running on Optimism, Positioning, and Thin Liquidity

Barron’s frames the rally as a “triple dose of summer optimism,” with stocks surging and traders asking if June can finish strong. That’s the right question for late June: liquidity thins, volatility can compress, and moves get exaggerated.

The fuel is familiar: resilient macro prints, hope that inflation stays contained, and a market that keeps treating AI capex as the new profit cycle. Add systematic flows and buybacks, and you get levitation — even when the news is merely “not bad.”

But rallies built on sentiment and positioning can reverse fast when a single input changes: a hot inflation print, an ugly auction, or a policy headline out of Washington. The higher the index goes, the less it can tolerate surprises.

📈 Fred's Take: Yes, stocks can finish June strong — the path of least resistance is still up while data holds and liquidity stays friendly. But you don’t chase beta here; you buy what you’d be willing to hold through a 5–7% air pocket. Keep some cash, keep your hedges cheap, and let the tape prove it can handle higher rates without cracking.

📎 Barron's

Venezuela Quakes, Micron Pops AI, and the Reminder: Supply Chains Still Matter

Bloomberg’s audio roundup flags deadly earthquakes in Venezuela alongside Micron helping buoy the AI trade. Two separate items, one unified market truth: physical-world shocks and compute-world demand are both steering prices.

Natural disasters hit commodities, logistics, insurance, and sovereign risk. Even when the immediate macro impact looks localized, markets re-price risk fast when infrastructure, ports, or energy systems are threatened. Meanwhile, Micron’s lift is the other side of the economy: memory and data infrastructure are back as core beneficiaries of the AI buildout.

Put it together and you get the current regime: industrial resilience plus AI capex plus periodic “real-world” disruptions. That’s why dispersion stays high — and why stock-picking keeps beating lazy index narratives.

📈 Fred's Take: Micron strength is a tell: the AI trade isn’t just GPUs, it’s the entire memory/storage/power stack. But don’t ignore the Venezuela headline — disasters create sudden inflation pockets and credit stress, and those spill over through commodities and insurers. Own the AI enablers, but keep one eye on physical risk that can whipsaw rates and energy.

That’s the board. Stay liquid, stay hedged, and don’t confuse a quiet summer tape with low risk. — Fred Frost

— Fred Frost