Today’s Sponsor

Three under-the-radar small-cap stocks are showing early signs of unusual market activity. Our research team has identified emerging changes in volume patterns and momentum that typically precede broader market attention.

These lightly covered companies are just starting to appear on institutional watchlists. Get our complete analysis covering where the activity is happening, what's driving participation, and our criteria for tracking these emerging setups — releasing in the next 24-48 hours.

Get the Free Research UpdateThis material is shared strictly for educational and informational purposes. We encourage readers to perform their own research and due diligence. By clicking the link you will automatically be subscribed to the Stock News Trends Newsletter. Privacy Policy

Image via MarketWatch

Madison Air’s $2.2B IPO: The Biggest Industrial Debut Since 1999

Madison Air just raised $2.2 billion in its IPO—largest deal of the year so far, and the biggest industrial-sector IPO since 1999. That’s not just a headline: it’s a risk-on signal in a market that’s been picky about who gets capital and at what price.

The “air-quality” angle also matters. If Madison Air sits at the intersection of industrial capex and regulatory compliance, it can ride both private-sector retooling and the constant churn of mandates from Washington and blue-state regulators. Investors are clearly willing to pay for scale and recurring demand.

✍ My Take: Big IPOs like this are liquidity magnets—and they usually pull attention (and dollars) away from small-caps for a while. If you’re long industrials, treat this as confirmation that the capex cycle is alive, but don’t chase the first-week pop; industrial IPOs can be brutally mean-reverting once the bookrunners are done “supporting.” I’d rather own profitable incumbents in the same supply chain than gamble on fresh paper priced for perfection.

Image via Fox News

GOP Leans Into Bigger Refunds: The “It’s Your Money” Trade Returns

Republicans are turning tax refunds and new deductions into a midterm message: working Americans should feel relief in their paychecks and at filing time. Blue states are resisting parts of the relief push, setting up another round of federal vs. state tax friction—especially where SALT caps, deductions, and compliance complexity collide.

Markets care because tax policy isn’t just politics—it’s consumption math. Bigger refunds can act like a mini-stimulus for retail and services, even if it’s really just timing (people over-withheld, then got “paid back”). The more Washington pushes “refund optics,” the more you should expect policy to skew toward demand support rather than deficit restraint.

✍ My Take: Near-term, this is modestly bullish for consumer-facing names—but it’s also another sign neither party is serious about spending discipline. If tax relief comes without real cuts, Treasury issuance stays heavy, and long rates stay stubborn. I’d keep duration short, favor quality dividend payers, and avoid assuming “refund season” permanently boosts discretionary spending.

📎 Fox News

Image via Washington Examiner

Mamdani Keeps a Line to Trump: NYC’s “Pragmatism” Meets Bond Reality

New York City Mayor Zohran Mamdani says he remains in touch with President Trump despite major disagreements, highlighting collaboration even amid contentious national security politics. The real story for investors isn’t vibes—it’s leverage. When big-city executives signal they can work with the White House, it affects federal funding expectations, regulatory posture, and the tone around municipal backstops.

NYC sits at the crossroads of public safety, immigration costs, commercial real estate stress, and a tax base that can move. Any hint of improved federal-city coordination can tighten muni spreads at the margin—especially for issuers with headline risk. But it can just as easily become a political football that raises uncertainty.

✍ My Take: Don’t confuse “staying in touch” with a durable fiscal fix. If you own NY munis, you’re still underwriting governance, pension reality, and office-vacancy math—not press conference diplomacy. I’d stay selective in big-city muni exposure and prefer essential-service revenue bonds over anything that depends on rosy budget assumptions.

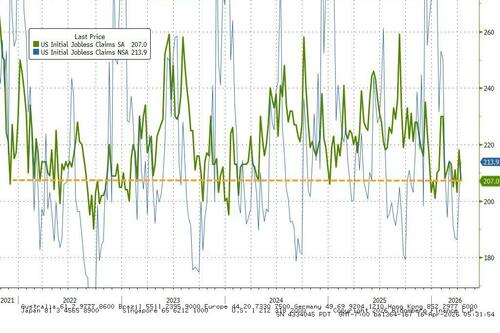

Image via ZeroHedge

Jobless Claims Near Lows: The Fed’s “Higher for Longer” Fuel Stays Lit

Initial jobless claims reportedly fell to about 207K—near historic lows—despite souring sentiment surveys. That’s the split screen markets keep grappling with: people *say* they’re worried, but the labor market keeps refusing to crack.

For investors, this matters because the Fed watches hard data first. Low claims keep wage pressure alive, keep services inflation sticky, and make it harder for policymakers to justify aggressive cuts. The “soft landing” narrative stays intact—until it doesn’t.

✍ My Take: This is not what rate-cut bulls want to see. Strong labor data supports earnings, but it also supports tighter financial conditions for longer—especially in long-duration tech and over-levered real estate. I’d stay overweight cash-flow businesses and underweight “promise stocks” that need falling yields to work.

Stay disciplined—policy noise is loud, but cash flow and rates still run the tape.

— The Morning Bullets Desk